You did the work, delivered the project and sent the invoice. Now all that's left to do is get paid. But if your customer is in another country, that last step may cost you more than you imagine. Bank fees, exchange rate spreads and waiting days are real frictions that reduce your real income. Here we explain how the system works and what options you have to make better payments.

The problem of charging for traditional banking

When a customer abroad transfers money to you through the conventional banking network, the process goes through the system SWIFT: a chain of intermediary banks that moves money between countries.

The result in practice:

- Reception fees: between USD 20 and USD 40 per transfer, plus additional percentages depending on the amount.

- Exchange rate spread: banks apply a margin of between 2% and 4% on the real interbank exchange rate. For a transfer of $3,000, that can mean between $7,000 and $14,000 CLP in difference.

- Waiting time: between 2 and 5 business days, depending on the intermediary banks involved.

- Bureaucracy: for large amounts, banks may request additional documentation that further delays the process.

For someone who charges two or three times a month, those costs add up significantly to the year.

What alternatives are there?

The international payments market has evolved considerably in recent years. Today there are platforms that allow you to receive payments from abroad with lower costs, greater speed and more transparency.

Return is one of those solutions, designed specifically for the Latin American market and based in Chile. This is the real comparison:

AttributeTraditional Banking (SWIFT) ReturnsReceiving FeesUSD 20—40 + percentagesCompetitive rates, no hidden chargesDelivery time 2 to 5 business days95% of payments in less than 30 seconds Exchange rate Bank spread from 2% to 4% Transparent rates calculated in real time SupportBureaucracy, physical presence or telephone waiting24/7 personalized service via WhatsApp

What coins can you receive?

The most common currencies for international payments from Chile are the U.S. dollar (USD) And the euro (EUR). Both can be settled in Chilean pesos (CLP) depending on the observed exchange rate.

It is important to understand that even if you receive in dollars, the internal accounting record in Chile must reflect the equivalence in CLP at the date of receipt of the income, for the purposes of PPM and income tax return.

Operational limits by country

To maintain regulatory compliance, payment platforms set limits that vary depending on the country of origin of the payment. In the case of Retorna:

Destination Country Suggested Monthly Limit Method United States Bank Transfer Up to USD 3,000 Spain (EU) SEPA Transfer Up to EUR 5,700 Peru Banks or Wallets (Yape) Up to USD 5,000 Colombia Banks or Cash According to customer profileArgentina Bank Transfer Up to USD 84,000 per year

These limits cover most of the operations of freelancers and consultants. For larger amounts in corporate transactions, the compliance team can enable customized quotas upon submission of documentation.

How regulation protects your money

One of the most important factors when choosing a collection platform is knowing that it is supervised. Retorna Holding SpA operates under the supervision of Chile's Financial Analysis Unit (UAF), which ensures that money flows are monitored and comply with national anti-money laundering regulations.

In addition, the platform employs advanced security protocols to protect your personal and financial information.

The full cycle: from the bill to the money in your account

For a freelancer or consultant who exports services, the ideal process is:

- Issue the Electronic Export Invoice on the SII portal with the generic RUT 55.555.555-5.

- You send the invoice to the customer in PDF by mail.

- The customer makes the payment in USD or EUR through the platform you have agreed to.

- You receive the funds in Retorna in minutes, with a transparent exchange rate.

- Liquids in Chilean pesos direct to your bank account.

- You declare income on your monthly F29 and you accumulate tax credit to request a VAT refund with the F3600.

Each step of the process can be efficient or costly, depending on the tools you choose.

FAQs

Do I need a dollar account in Chile to collect from abroad?

It's not mandatory, but having a foreign currency account can make it easier to manage if you receive recurring payments in dollars and don't want to settle everything right away. With Retorna you can receive and decide when to convert.

What information do I need to give my customer to get paid?

It depends on the method. For SWIFT transfers you need the bank's SWIFT code, account number and bank address. For alternative platforms, the data varies by system.

Can I charge partially in advance payments and the rest when delivering?

Yes. In that case, you must issue the invoice when the price is agreed or when you receive each payment, as appropriate. Check with your accountant for the correct timing for each installment.

What happens if the exchange rate falls between when I issue the invoice and receive the payment?

It's a risk inherent to working in foreign currency. Some platforms allow you to set the exchange rate at the time of collection. Alternatively, you can consider adjusting your rates to absorb potential variances.

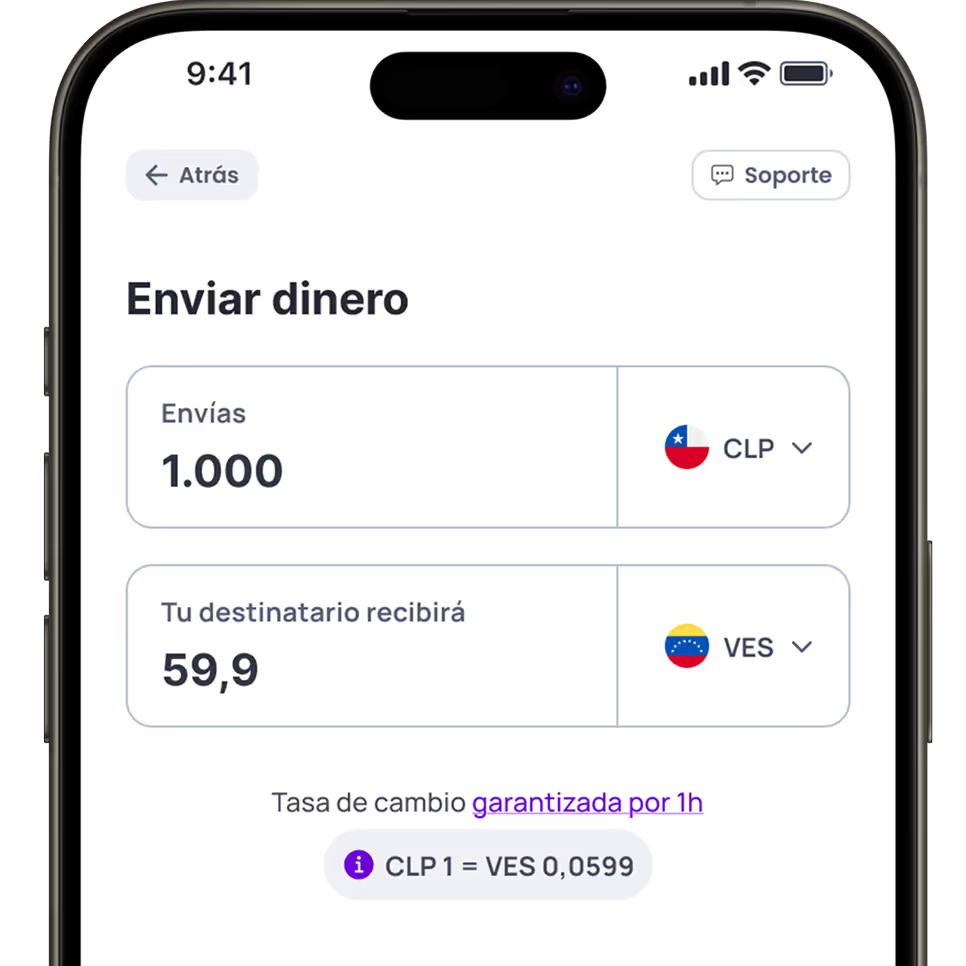

Your money arrives in a heartbeat

With Retorna, your transfers arrive in minutes. It's as easy as sending a WhatsApp message. Send money in just a few clicks—fast, secure, and hassle-free.

Escanea el código y empieza a enviar dinero a tus seres queridos en cualquier parte del mundo.

Disponible en